Debts and Relationships: How to Talk About Finances with Your Partner

Understanding Financial Dynamics in Relationships

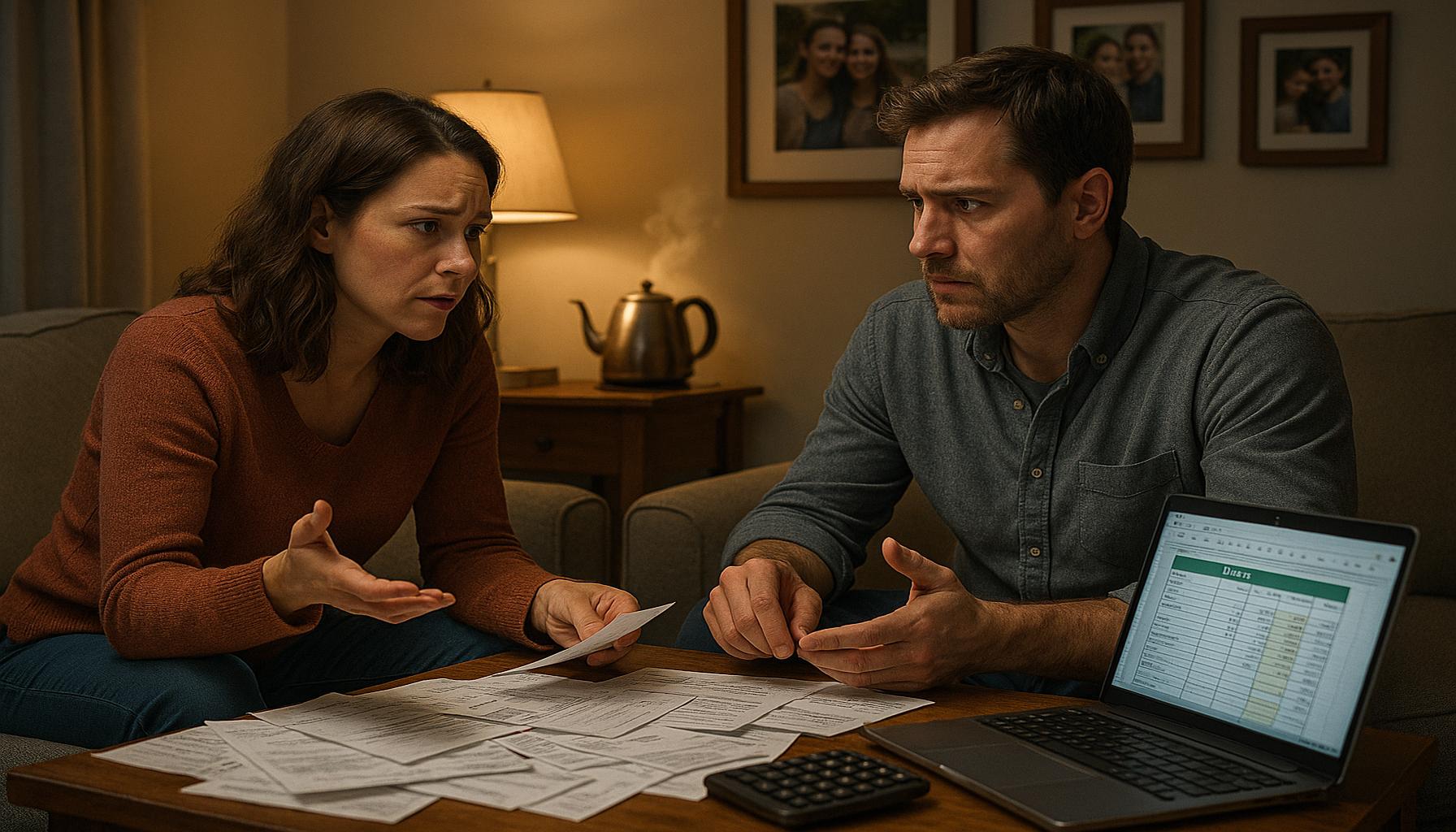

Effective management of finances is pivotal for the stability of any relationship. The complexities of debt management, spending habits, and financial planning can create considerable stress if left unaddressed. Research shows that approximately 70 percent of couples experience financial disagreements, making it essential to prioritize and facilitate discussions about money. Without clear communication and understanding, these financial issues can escalate into major conflicts, potentially leading to relationship breakdown.

Open Communication

A foundational step in financial discussions is establishing a culture of open communication. Couples should feel at ease discussing their financial standings, aspirations, and challenges. To foster this environment, consider scheduling regular financial meetings—perhaps monthly or quarterly—where both partners can voice their thoughts and concerns regarding money matters. Create an agenda for these meetings to ensure that all relevant topics are covered, such as budgeting, savings, and investments. This proactive approach not only normalizes financial discussions but also reduces the emotional burden of financial secrecy.

Shared Goals

Another crucial aspect of managing finances as a couple is setting shared goals. Having collective financial objectives, such as saving for a house, planning a vacation, or preparing for retirement, encourages teamwork and commitment. Goal-setting should involve a candid discussion about each partner’s visions and priorities. For instance, if one partner is focused on saving for a new car while the other envisions an international trip, finding a middle ground can lead to compromise and collaboration. Additionally, tracking progress toward these shared goals together can enhance accountability and reinforce the partnership’s unity.

Understanding Debts

Moreover, it is vital for each partner to have a clear understanding of the other’s debts and financial history. Addressing existing debts before tying financial futures together can prevent misunderstandings and resentment. Couples should take the time to disclose their debts—whether they are student loans, credit card balances, or mortgages—along with their strategies for managing them. For instance, one partner may propose setting up a debt repayment plan that outlines monthly contributions or the snowball method to pay off smaller debts first. This transparency fosters trust and equips both partners to make informed financial decisions together.

Financial issues remain a significant contributing factor to relationship dissatisfaction in the United States, underscoring the need for proactive financial management. By focusing on constructive dialogue, couples can mitigate potential conflicts and enhance their emotional bond. Learning to navigate each other’s financial landscapes not only encourages healthier financial habits but also cultivates a stable and supportive partnership. Implementing these strategies equips couples with the necessary tools for sustainable financial success, positively impacting their overall relationship dynamic.

DISCOVER MORE: Click here for tips on organizing your finances

Navigating Financial Conversations: The Importance of Clarity and Transparency

When discussing finances in a relationship, clarity and transparency serve as the cornerstones of healthy communication. It is often the case that one partner may have a different understanding of financial situations than the other, leading to confusion and potential conflict. To bridge this gap, couples should approach financial discussions with the intent to share as much information as possible. This means discussing not only income but also any outstanding debts, spending habits, and any financial obligations each partner may have.

Types of Debts to Discuss

Both partners should be prepared to openly discuss various types of debts that may impact their financial landscape. Below is a list of common debt categories worthy of scrutiny:

- Student Loans: Understanding the amount owed and the repayment terms is crucial, particularly as these loans can impact future financial planning.

- Credit Card Debt: Since high-interest rates apply, discussing the total balances and payment strategies should be a priority.

- Mortgages: If either partner owns a home, clarity around existing mortgage payments and home equity is essential for joint budgeting.

- Medical Debt: Medical expenses can accumulate quickly and may require a tailored repayment plan if one partner faces significant medical bills.

- Personal Loans: This can include loans from friends or family, which may not appear on credit reports yet still impact financial obligations.

Couples should not only enumerate their debts but also elucidate their respective repayment strategies. For example, discussing whether they prefer to employ the debt snowball method, which focuses on paying off smaller debts first, or the debt avalanche method, which prioritizes debts with the highest interest rates, can provide insight into their financial priorities and problem-solving approaches.

The Emotional Impact of Debt Disclosures

It is also important to recognize the emotional impact that financial discussions can carry. Many individuals may feel shame or embarrassment regarding their financial situation, particularly if they carry significant debts. As such, partners must approach these discussions with empathy and support. Establishing a respectful dialogue can help mitigate feelings of judgment and stigma, thus fostering a stronger partnership in the face of financial challenges.

By initiating these crucial conversations around debt management, couples not only set the groundwork for a shared financial future but also strengthen their emotional bonds. Addressing these discussions head-on provides clarity, encourages responsibility, and reinforces a sense of teamwork, essential for any successful relationship.

In summary, navigating the waters of financial discussions requires intentionality, openness, and understanding. Cultivating an atmosphere where both partners feel comfortable discussing their debts can significantly ease the pressure surrounding financial issues, allowing couples to focus on building a future together. In the current economic climate, where financial disputes often lead to relational strain, placing an emphasis on these conversations is not merely advisable; it is necessary for enduring partnership success.

DISCOVER MORE: Click here to unlock the full potential of your premium credit card

Building a Financial Plan Together: Setting Goals and Responsibilities

After establishing a foundation of clarity and transparency regarding debts, couples should focus on creating a joint financial plan that encompasses shared goals and responsibilities. This approach promotes collaboration and accountability, enabling partners to work towards a common vision for their financial future.

Identifying Financial Goals

The first step in building a financial plan involves identifying financial goals. These goals can vary significantly among individuals and may include short-term aspirations like saving for a vacation or purchasing a new vehicle, as well as long-term objectives such as buying a home, funding children’s education, or planning for retirement. Couples should set aside time to engage in discussions about their priorities, using the SMART criteria—Specific, Measurable, Achievable, Relevant, and Time-bound—to articulate these goals effectively.

For example, a couple might decide that they want to save $20,000 for a house down payment within five years. This specific goal can provide both partners with a target to strive towards, making it easier to allocate resources appropriately and stay motivated.

Creating a Budget that Reflects Mutual Interests

Once goals are established, couples should work together to create a budget that reflects their shared financial objectives. A well-structured budget not only tracks expenses and income but also allocates funds toward debt repayment and savings. Couples can adopt various budgeting methods, such as the 50/30/20 rule, which allocates 50% of income to needs, 30% to wants, and 20% to savings and debt repayment. This systematic approach can help couples prioritize their financial commitments while ensuring that both partners’ interests are considered.

Moreover, budgeting needs to be dynamic. Financial circumstances often change due to promotions, job losses, or unexpected expenses. Couples should schedule regular check-ins—monthly or quarterly—to review their budget, assess progress toward financial goals, and adjust as necessary. These discussions maintain a proactive approach to financial management and can reinforce a sense of teamwork.

Assigning Financial Roles and Responsibilities

Assigning clear roles and responsibilities in managing finances can also streamline the process. This division of labor can alleviate stress by ensuring that both partners know who is responsible for specific tasks. For instance, one partner may take charge of paying monthly bills, while the other may focus on tracking investments and savings. Clearly defined roles can help couples avoid potential misunderstandings and promote accountability.

It is crucial, however, that both partners maintain an understanding of overall financial health. Regular discussions about monetary matters, even if one partner is primarily responsible for managing them, help ensure transparency and mutual respect. This comprehensive engagement fosters a sense of participation and collaboration, vital for maintaining a healthy financial relationship.

Handling Financial Disagreements with Respect

Financial conversations can sometimes lead to disagreements, particularly when partners have differing values or habits related to spending and saving. It is essential for couples to approach these discussions with respect and an open mind. Utilizing “I” statements, such as “I feel concerned when our spending exceeds our budget,” can help both partners express their feelings without causing defensiveness.

Additionally, seeking external assistance, such as a financial advisor, can offer neutral guidance and craft a polished plan that addresses both partners’ perspectives. Working towards a financial strategy should never be a battle; instead, it should be a partnership enriched by understanding, communication, and commitment. This collaborative mindset can transform financial challenges into opportunities for mutual growth, strengthening not only the couple’s financial well-being but also their emotional connection.

DISCOVER MORE: Click here for all the details

Conclusion

In summary, discussing debts and finances with a partner can be a challenging yet essential aspect of nurturing a healthy relationship. By fostering a culture of transparency and open communication, couples can navigate the complexities of financial management together. Establishing a joint financial plan that includes clearly defined goals is an effective strategy that encourages collaboration and enhances overall accountability.

Understanding each partner’s financial aspirations and limitations is paramount. By identifying mutual financial goals and creating a budget that reflects shared interests, couples are not only more likely to achieve their objectives but also foster a deeper emotional connection. Equally important is assigning roles and responsibilities in financial management to ensure that each partner feels engaged and accountable, while also enabling a thorough understanding of their collective financial health.

When disagreements arise, approaching discussions with respect and empathy allows partners to address conflicts constructively. Utilizing tools such as “I” statements can further facilitate healthy dialogue, ensuring that both partners feel heard and valued. By prioritizing flexibility and ensuring regular check-ins on financial matters, couples can adapt to changing circumstances and reinforce their partnership.

Ultimately, the process of managing debts and finances can strengthen a relationship when approached with a shared vision, communication, and mutual respect. By transforming financial challenges into opportunities for growth and collaboration, couples can cultivate both their financial stability and emotional intimacy, positioning their relationship for long-term success.

Related posts:

How to Handle Financial Emergencies Without Getting Into Debt

The Impact of Financial Education on Personal Debt Management

How Debt Negotiation Can Improve Your Financial Health

Best practices for using a credit card without falling into debt

Effective Strategies to Reduce Credit Card Debt

How to Shop Consciously and Avoid Impulse Spending

Linda Carter is a writer and financial expert specializing in personal finance and financial planning. With extensive experience helping individuals achieve financial stability and make informed decisions, Linda shares her knowledge on the our platform. Her goal is to empower readers with practical advice and strategies for financial success.